How bad is the fall of Euro. Does the Euro-zone crisis marks the beginning of the end for the European currency? Will Euro ever recover? Is it in Greece’s interest to default and leave the Euro-zone? How do we even begin to answer these questions?

I have lived in a country that has faced a major currency crisis once every decade, sometime even more. Growing up I remember the dollar trading at an exchange rate of 20 rupees to a US dollar, which somehow unexplainably became 40 (in the early 90’s) then 60 (late 90’s) then 68 (the 1998 nuclear explosion embargo and crisis). Then years of stability followed from the turn of the century to mid 2008 when the once in a decade crisis arrived again and we saw a hellish ride to 86 from 62 in a span of a few months.

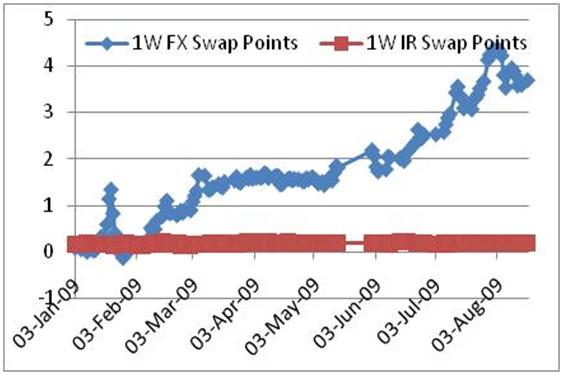

One of my favorite measures of FX outlook is the swap point curve. How much would it cost you to exchange a unit of currency in the future? From your desktop model? For real in the market? Here is the swap point data for PKR again USD, post the currency crisis in 2008. The model predicted a point for a week long forward quote; the market priced it at 4 times as much.

In essence what that meant was that as an importer you had little or no protection or as my treasury counterpart put it (you were truly French Connectioned in UK) and as an exporter you really didn’t care.

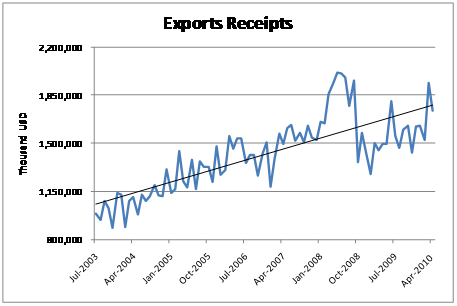

Here is what the crisis did to our national monthly exports figures

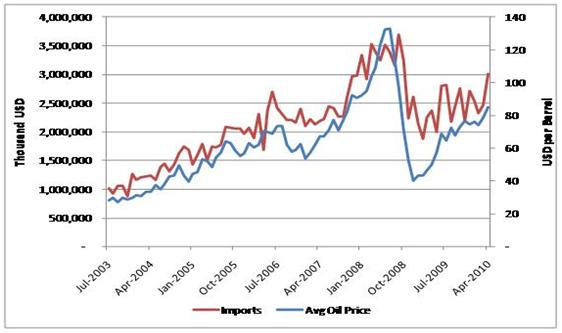

And our imports.

Notice the steep fall in October 2008 when the crisis and oil prices peaked. Exports fell from a monthly rate of about 2 billion dollars to 1.35 billion US. Imports fell from 3.5 billion US dollars to 2 billion US.

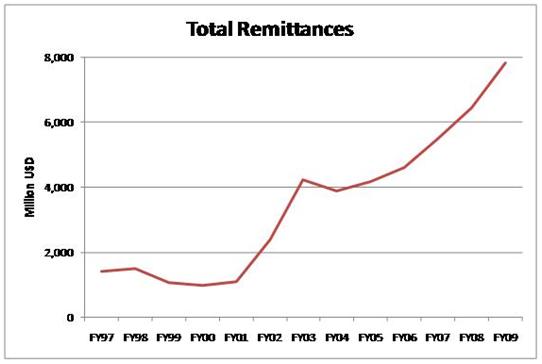

And our worker’s remittances

Currency devaluation is a textbook cure for ailing economies that need to get on the fast track to austerity drives and fix their balance of payment problems. Imports get more expensive, exports get more competitive and the cheaper currency internationally creates incentives for international workers to send more money back home. While the Euro is a more complex study in terms of the number of economies involved, but the text book cure should technically also work here.

The only problem with the text book cure is that foreign currency loans and debt get more expensive to service as we found out in 2008 and the rest of Asia discovered in 1997. But since the 110 billion dollar Greece package is Euro denominated, as long as Greece remains a member of Euro, it will be spared the debt exchange impact.

Hence the reluctance of the ECB and Mr Juncker to defend the steep fall in Euro. They are right, as per the plan the Euro doesn’t need a defense. The steep fall in the value of Euro is exactly what the doctor prescribed for the zone. Import less, export more.

Still the expectation right now is that at the rate we are going, we will see a dip to 1.18, maybe 1.19 to a dollar in the coming weeks before the Euro really bottoms out. In the long run it will work out for Europe, Eurozone and Euro. In the short run there is going to be nothing but pain.

[ad#Grey back med rectangle]