Crude Oil Macroeconomic forecast model

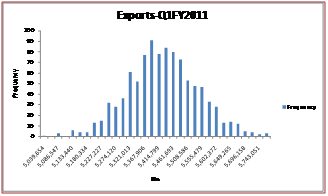

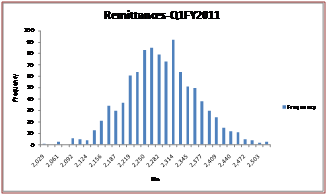

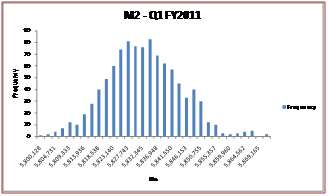

Given the nature of our economy, one key factors effecting the economic outlook of Pakistan is the country’s balance of payments in particular the balance on its current account. In turn the major factor impacting the surplus/ deficit of the current account has been its sensitivity to oil price changes due primarily to increased imports in crude oil and related products. The current account surplus (increase in net foreign assets) impacts M2 growth which in turn effects inflation and plays a role in the determination of the central bank’s policy rate.

The ranges of results for the first quarter of fiscal year 2010 – 2011 from our macroeconomic forecast model’s simulated runs are as follows:

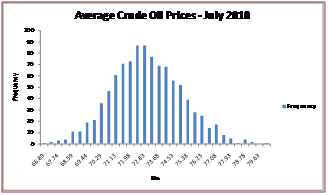

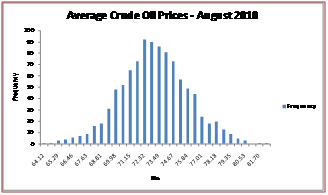

The crude oil outlook for the first quarter of the new fiscal year

|

|

|

|

|

The impact of crude oil prices on the economy

|

|

|

|

|

|

|

|

|

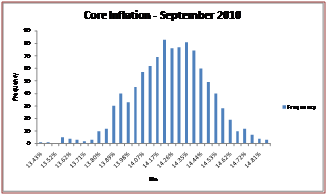

Generally as inflation increases monetary policy is tightened and the policy discount rate is increased. The opposite happens when inflation declines- the monetary policy is relaxed and the policy discount rate is cut. Assuming a minimum difference between the policy discount rate and the core inflation rate of 0% and no attempt made to further tighten the monetary policy (i.e. a policy rate increase is not on the cards) then under all the simulation runs above there will be no cut in the policy discount rate and it will be maintained at 12.5%. |